In this lesson, I want to talk to you about trading Short Strangles during a market crash.

We get this question from our members all the time. “Yeah, the strategy is working great now, but what happens if we have a crash like we did in 2008?”

Many times newer traders have a fear of trading naked options. They think, “Oh my gosh, if 2008 happens again I could lose all of my money.”

We completed an in-depth study to determine the outcome.

Criteria for Our Back Tested Study

Let’s go over the criteria we used in this study.

We’re looking at the S&P 500, or SPY.

We’re entering these short strangles with 45 days left to expiration. We typically like to enter anywhere from 30-60 days, so 45 days is right in the middle.

We closed our winners at 50% of max profit.

And we looked at a couple of different timeframes.

We looked at the most recent five years. This time period was a pretty outstanding bull market, and so you would think that Short Strangles would have done well because if the market goes up, implied volatility is contracting, potentially giving you profit. So, we wanted to look at that and compare that to the market crash.

In 2007-2009, we saw one of the most volatile markets, the biggest market meltdown that we’ve ever seen, and so I want to take a look at how the performance of the Short Strangles did during those two periods. To do that, we’re going to go to the CML Option Strategy Backtester, the CML trade machine.

CML Option Strategy Backtester

On the sidebar to the left, we’re looking at trading a Strangle, so let’s select “Strangle” from under Strategies.

We’re selecting “Short”, because we’re selling.

Obviously, with SPY, there are no earnings. It’s an ETF, so we’re just going to click “Nothing Special” from under Earnings Handling.

We’re going to open the trade in “Normal Time”.

We’re going to close the trade when we have gains at 50% of max profit.

Then, we’re going to open our next trade immediately. So as soon as we take one off, we’re going to open a new one.

Keep in mind, this is not even taking into consideration implied volatility. We are placing these trades whether implied volatility is low or high, it doesn’t matter.

5 Year Study

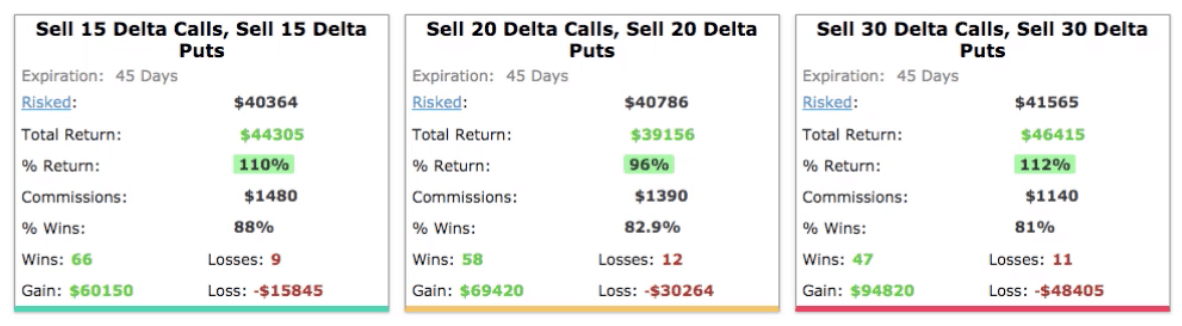

I want to start with the five-year study, going back the most recent five years. Typically, when we sell Strangles at NavigationTrading, we’re playing in the 15-30 delta range. We’re selling the 15 Delta, 20 Delta, 30 Delta, somewhere in there.

I went ahead and added the 40 Delta and the 50 Delta. The 50 Delta, would essentially be a Short Straddle. These are just here for your reference.

Going back to the 15 Delta, 20 Delta, and 30 Delta, what you’ll see during the last five years, is that Short Strangles performed really well. We see high win rates at 88%, 82%, and 81%. So, very high win rates, making it a profitable strategy.

Keep in mind, if we were just putting these on during high implied volatility, these numbers would be even better. We’ve been talking to Ophir and his team at CML about adding that implied volatility filter. It’s not in the software yet, but hopefully, it will be in the future and we’ll be able to see how much that enhances the returns even more.

2007-2009 Study

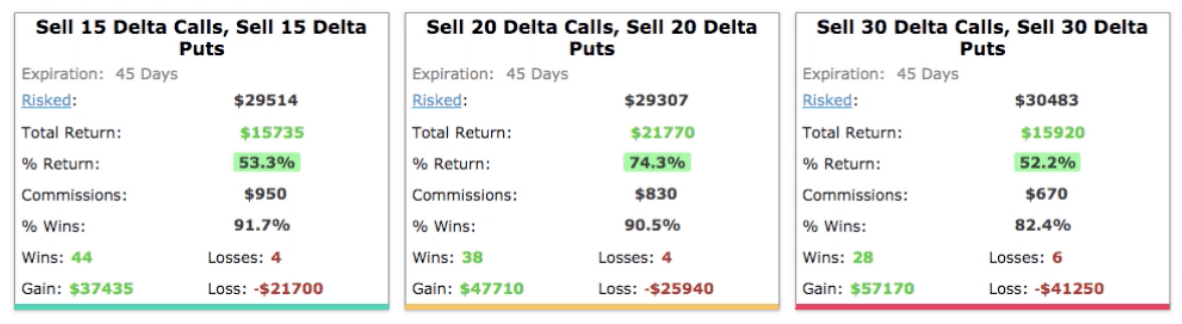

What about during the 2007-2009 timeframe?

Again, this was one of the most volatile times we’ve ever seen. It was one of the biggest market crashes we’ve ever seen. Let’s see how Short Strangles performed during this period.

When you’re selling a Strangle, these are naked options. The risk is theoretically undefined. The key is to keep your position size small, relative to your account size, and to continue to put these trades on, just like we’re showing in this study.

In this case, we’re just putting one on, and as soon as it closes, we’re putting on another, that one closes, we’re putting on another one. This study just helps give you an idea of how that has performed.

Look at how this strategy has performed with the 15 Delta. It made a return of over 53%. It had over a 91% win rate.

The 20 Delta made a return of over 74%, with over a 90% win rate.

The 30 Delta made a return of over 52%, with an 82% win rate.

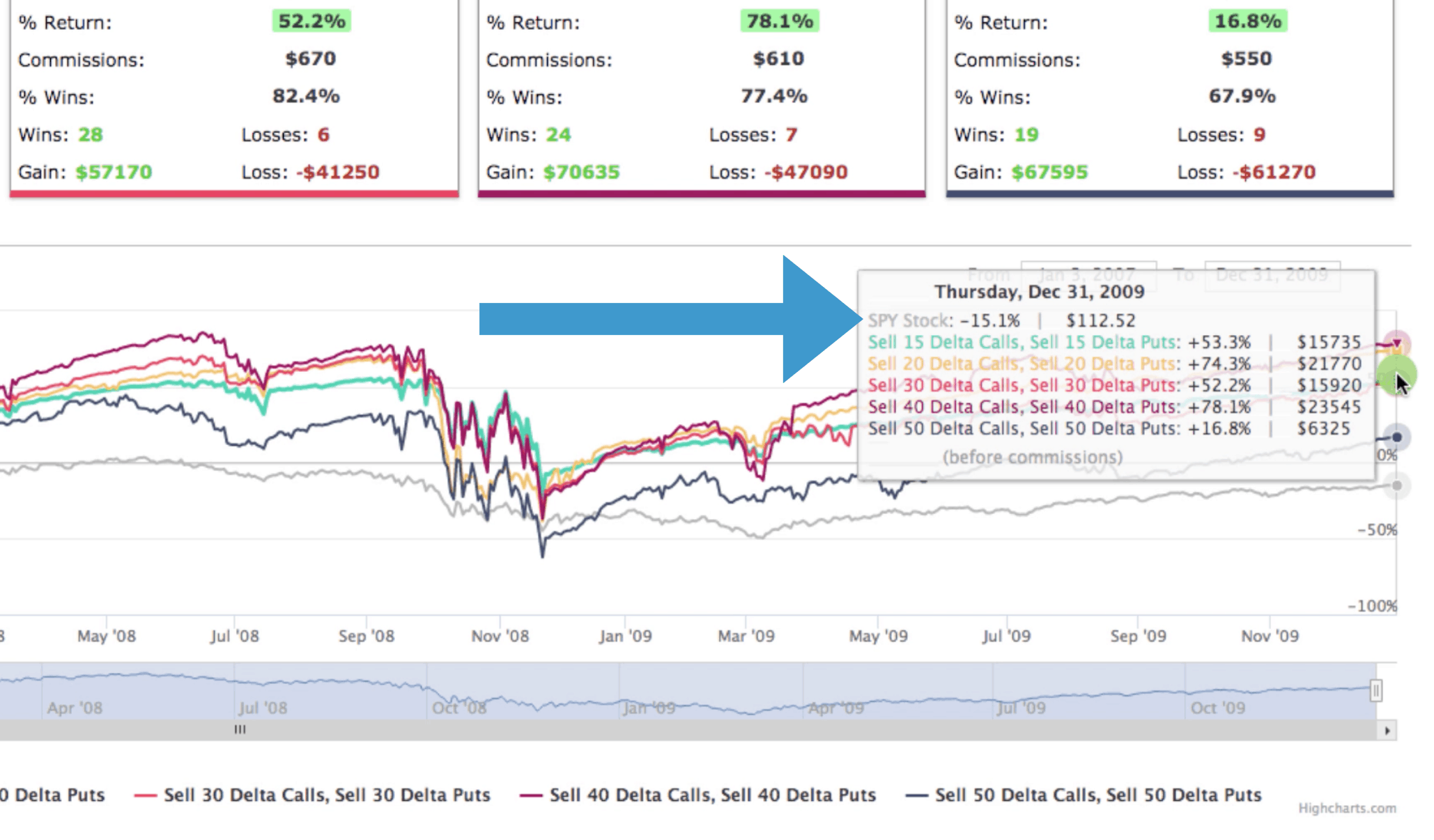

Then, you can see the 40 and the 50 Deltas were positive as well.

Takeaways

If I hover over the graph at the bottom, you can see a box pops up showing you that over that period of time the S&P 500 was down 15.1%. Every other Short Strangle, regardless of the Delta you chose, was positive. They were significantly more positive. The results weren’t as good as it was in a Bull market, but it was still positive, and it beat the pants off the S&P 500.

So, if you’re comparing this to investing in mutual funds or buying index funds, now you see how this strategy has performed. Just by doing this simple option strategy, putting a Strangle on, taking it off, putting a Strangle on, taking it off, you beat the pants off of the S&P 500.

The reality of this strategy is, where there’s perceived risk of having uncovered options, naked options, theoretically unlimited risk during one of the biggest market meltdowns, it still is profitable.

Again, this isn’t even taking into consideration picking and choosing when we put these on, where we get to pick and choose only putting them on in high implied volatility. This is putting them on in high implied volatility and low implied volatility, just putting them on one after another.

I hope this was helpful in just showing you the power of what this backtesting strategy can help give you, not only from a confidence standpoint but overall just finding your opportunities.

If you’re interested in getting your own access to this software, to the CML Trade Machine Pro, we have worked out a deal with Ophir Gottlieb and his team at CML, to get our member’s a discounted rate. Normally, the software is $149 a month (that price just went up, it was $129). As he continues to put additional resources and value in the software, that price will continue to go up. However, for NavigationTrading members, he has given us a special offer of over 40% off, at just $89 a month. If you’re interested in checking that out and learning more, there’re some videos there on this page. Just go to cmlviz.com/navt.

Hope this was helpful. We’ll talk to you next time!

Happy Trading!

-The NavigationTrading Team

Follow